Last week the Treasury Department released year-end spending and revenue numbers for Fiscal Year 2024, showing a budget deficit of $1.8 trillion. On the surface, that’s an increase of $138 billion over the 2023 deficit, but the 2023 deficit was artificially lowered by about $300 billion due to an accounting adjustment reflecting the Supreme Court’s rejection of the Biden Administration’s student debt loan forgiveness plan. Without that adjustment, the 2023 deficit was $2 trillion and the 2024 deficit was actually almost $200 billion lower than in 2023. As a share of the gross domestic product (GDP), the deficit in 2024 was 6.4 percent, up from 6.2 percent in 2023, but lower than the adjusted 2023 figure, which the Treasury says was 7.4 percent of GDP.

This accounting may seem a bit confusing, but the bottom line is that the 2024 deficit was very, very big. Without a major calamity such as war or economic disruption, a deficit of 6.4 percent of GDP is highly unusual and should be a cause for alarm. Yet on the campaign trail, we hear little about the deficit except when it is used to blame the other side for fiscal malfeasance.

We are deeply into uncharted territory. The Congressional Budget Office (CBO) reports that since at least 1930, deficits have not remained above 5.5 percent of GDP for more than five years in a row, but CBO projects deficits at that level and above for every year throughout the next three decades, far exceeding the average over the past 30 years (3.8 percent). In other words, we’re now running deficits at 6 percent of GDP and higher as a routine matter. What was once a major anomaly is now the norm. By 2054, CBO projects that the deficit will reach 8.5 percent of GDP.

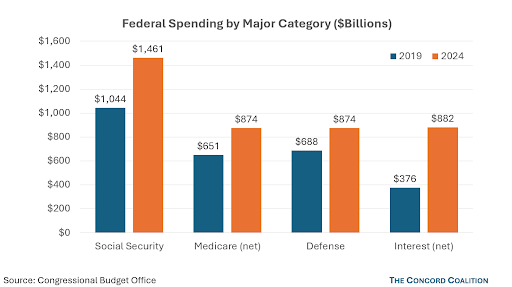

Perhaps one number in the Treasury Department’s report will get the attention of those seeking to lead our nation: Net interest on the debt spiked in 2024 to $882 billion from $659 billion in 2023, and has more than doubled from $376 billion in 2019. That dramatic increase places net interest above defense spending and Medicare, which were both $874 billion in 2024, as the second largest Federal expense behind Social Security ($1.46 trillion).

Regardless of who wins in November, the relentless growth of debt will still be there to greet them as they assume office in January. The problem is not episodic. It is structural. We have a widening gap between spending and revenues. Over the next 30 years, the CBO projects that mandatory spending (mostly entitlements) is projected to grow by 2.3 percent of GDP. Revenues are projected to grow as well, but only by 1.3 percent of GDP.

Widening deficits means growing debt. In 2027, during the next presidential term, federal debt held by the public, at 106.2 percent of GDP, is projected to exceed the highest level in U.S. history, which came at the end of World War II. By 2054 the debt level is projected to reach 166 percent of GDP. Again, we are traveling into uncharted territory.

Even that dire projection is probably optimistic because it assumes that the 2017 “temporary” tax cuts will expire rather than become permanent, and that annual discretionary spending will decline to an historically low level as a share of GDP.

It is an abject failure of leadership that a nation with all the advantages, ingenuity, and resources we enjoy has not acted to remedy, let alone barely acknowledge, the perilous fiscal crisis we face. The Federal budget is on an unsustainable path. This dynamic was created through legislative action – and inaction – and it will take legislative action to set a more sustainable course. The sooner these actions are taken, the better the chances of success. Kicking the can down the road means that solutions will be even more difficult and leaves more of the burden to be borne by future generations.