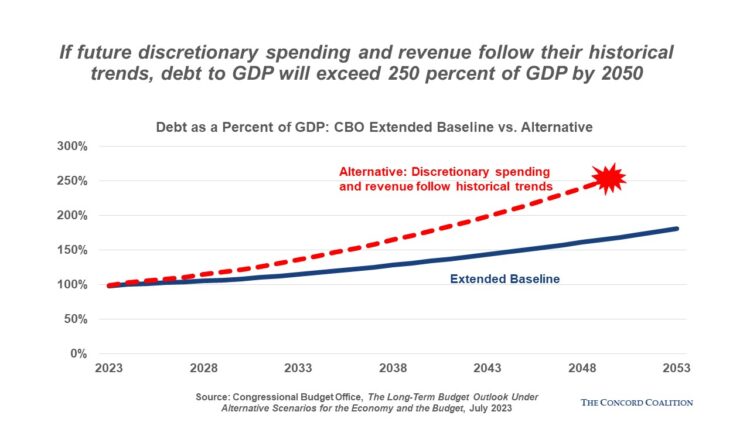

A new analysis by the Congressional Budget Office (CBO) suggests that if history is any guide, our nation’s debt could become far more burdensome over the next 30 years than projected under current law. That’s an alarming prospect because the debt is already projected to nearly double over that time, reaching a record shattering 181 percent of the gross domestic product (GDP) in 2053.

Standard CBO baseline projections assume that current laws regarding spending and tax policy remain unchanged. The 30-year projection is called the “extended baseline.” Because appropriations (discretionary spending) are enacted on an annual basis, CBO assumes that they will grow with inflation from the most recently enacted level over the next 10 years and then gradually transition to grow at the same rate as GDP growth.

Under these assumptions, CBO’s extended baseline projects that discretionary spending will shrink from 6.5 percent of GDP this year to 5.4 percent in 2053 and that revenues will grow from 18.3 percent of GDP this year to 19.1 percent in 2053. That combination has a positive effect on the budget, although not by nearly enough to prevent deficits and debt from continuing to rise beyond historical levels due to projected increases in mandatory spending, such as Social Security and Medicare, and growing interest on the debt.

In its recent analysis, CBO prepared an alternative scenario illustrating how the extended baseline would change if both discretionary spending and revenues equal the same share of GDP over the next 30 years as they have averaged over the past 30 years. Mandatory spending is assumed to grow as projected under current law.

By those measures, annual discretionary spending would be set at 7.1 percent of GDP, rather than averaging 5.7 percent as projected in the extended baseline, and annual revenues would be set at 17.2 percent of GDP, rather than averaging 18.4 percent as projected.

This is not an implausible scenario since it is based on past policy choices. The negative effect on the budget, however, would be dramatic. The combined result of higher discretionary spending and lower revenues, while consistent with the past 30-year average, would increase the projected debt in 2049 to 249 percent of GDP as opposed to 164.9 percent under the extended baseline. The CBO does not project a number beyond 250 percent of GDP because of “the significant uncertainty about the effects that such high levels of debt could have on the economy.”

To be sure, CBO concludes that there could be some long-term economic benefits from higher discretionary spending, such as more federal investments in research, development, and infrastructure. Lower revenues could also have economic benefits, such as encouraging more work, saving, and investment. However, these “pro-growth” benefits would be swamped by the negative economic effect of high and rising debt.

With Congress now considering proposals to either raise discretionary spending or cut taxes, this CBO alternative scenario serves as a useful reminder that current law – already unsustainable over the long-term – assumes just the opposite: a substantial decrease in discretionary spending and a substantial increase in revenues, relative to our recent past experience.

By implication, the scenario also demonstrates the folly of exempting mandatory programs from scrutiny. The historical 30-year averages strongly suggest that it will be difficult to achieve the discretionary spending cuts and revenue increases assumed in the baseline. Even more difficult, however, will be preventing demographic changes and healthcare costs from driving mandatory spending to much higher levels. Any realistic path to putting the budget on a sustainable basis will need a comprehensive approach.

This time, let’s hope the past ISN’T prologue.