Introduction

According to public opinion polls, the most popular way to “fix” Social Security is by taxing the rich, specifically by increasing or eliminating the limit on wages subject to the Social Security payroll tax.[1] Despite the populist appeal of this approach, it would have several offsetting effects on both Social Security and the federal budget that policymakers should not ignore.

This issue brief will examine the history and rationale behind the current taxable limit and consider how changing the limit would affect the Social Security program, federal income tax receipts, and the ability to address Medicare’s rising deficits.

Contribution and Benefit Base

Under current law, the Social Security payroll tax applies to annual wages (and net earnings from self-employment) up to $160,200.[2] However, the limit on the amount of wages subject to the payroll tax also serves to limit the amount of wages used to calculate benefits. Thus, the limit is more formally known as the “contribution and benefit base.”

As initially conceived in 1935 by President Franklin Roosevelt’s Committee on Economic Security, the Social Security payroll tax would have only applied to workers earning less than $3,000 per year.[3] (That amount was about 2.7 times the average wage.[4]) As enacted into law, the payroll tax was applied to the first $3,000 in annual wages. The shift from excluding workers earning above the limit to including them, but only taxing them up to the limit, was the result of competing views on program coverage.[5]

It was generally assumed that higher wage workers could save for their own retirement and thus did not need Social Security. However, the recognition that annual wages might rise above or fall below the limit during the year, or from one year to the next, led to concerns that some workers would intermittently gain and lose coverage throughout their career, resulting in inadequate retirement savings and reduced Social Security benefits. Thus, Congress decided to cover all workers up to the limit.[6]

The current limit is linked to the growth in average wages in the U.S. economy, resulting in an upward adjustment in the limit whenever beneficiaries receive their annual cost-of-living adjustment (COLA).[7] When there is no COLA, due to constant or falling prices as measured by the consumer price index (CPI), the limit remains unchanged.[8]

As noted above, the contribution and benefit base limits both contributions and benefits. For example, a hypothetical worker who turned 62 in 2023 and always earned the maximum taxable wage would have an average monthly wage of $12,427 and be eligible to receive a monthly benefit of $3,653, prior to any adjustments for early or delayed retirement.[9]

Eliminating the contribution and benefit base would result in workers paying taxes on all their wages, but it would also result in the payment of unlimited benefits. For example, workers with an average monthly wage of $83,333 – equivalent to $1 million per year – would be eligible to receive a monthly benefit of $14,289 – equivalent to $171,471 per year. Workers with higher wages would receive even higher benefits.

In the aggregate, eliminating the contribution and benefit base would increase annual Social Security taxes (including income taxes on benefits) by 20 to 25 percent, and increase annual Social Security benefits by 6 to 11 percent. Thus, every $1 of additional taxes would be offset by $0.40 to $0.64 of additional benefits. The range of estimates reflects the differences in assumptions and methods between the Social Security Administration (SSA) and the Congressional Budget Office (CBO).[10]

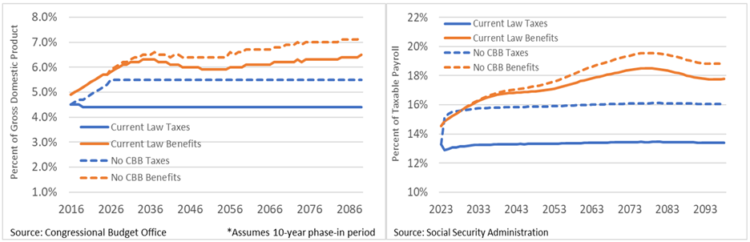

As shown in Figure 1, eliminating the contribution and benefit base (CBB) would not eliminate future Social Security deficits. Although the depletion of the Social Security trust fund would be temporarily delayed, benefits would continue to exceed taxes throughout the long-run projection period.[11]

Figure 1: Projected Social Security Taxes and Benefits: With and Without CBB

To avoid paying higher benefits to higher wage workers, Congress could break the link between taxes and benefits. However, taxing wages above the contribution and benefit base without providing any additional benefits represents a fundamental departure from Social Security’s tradition of linking both contributions and benefits to taxable wages.[12]

Proponents of eliminating the contribution and benefit base for the purpose of collecting more payroll taxes, but not for paying more benefits, often point to Congress’s decision to remove the limit on wages subject to the Medicare Hospital Insurance (HI) payroll tax in 1994.[13] They argue Medicare payroll taxes are unlimited, so why not Social Security? But that is not a valid comparison. Social Security taxes and benefits have always been linked to wages, while Medicare taxes and benefits have not.

The Medicare program has three parts: Part A hospital services, Part B physician and outpatient services, and Part D prescription drug coverage.[14] Only Part A is funded with a payroll tax, but its benefits are unrelated to wages. Parts B and D are funded with beneficiary premiums and general revenues. Any distinction between these parts is largely arbitrary. This has become even more apparent since the introduction of Part C Medicare Advantage plans in 2003. These plans, which now enroll nearly half of all Medicare beneficiaries, combine Part A with Part B, and sometimes Part D.[15] Part C plans receive funding on a capitated basis (i.e., per capita lump-sum), thereby eliminating any distinction between the source of funding and the mix of services provided to beneficiaries.

Unlike Social Security, which links benefits directly to wages, there is no connection between a worker’s wages and his or her Medicare benefits. According to a study published in the Journal of the American Medical Association in 2021, average annual Medicare spending per capita varies widely across the country based on geographic location and individual health status. Among fee-for-service beneficiaries, average per capita spending ranged from $4,447 in the country’s cheapest counties to $16,570 in the most expensive counties.[16]

According to self-reported health status data from the Agency for Healthcare Research and Quality (AHRQ), average per capita spending in 2021 ranged from about $4,000 among beneficiaries in excellent health to nearly $23,000 among beneficiaries in poor health.[17]

Figure 2: Average Annual Medicare Spending Per Capita (2021)

Finally, it should be noted that the HI tax rate is only 2.9 percent, plus an additional 0.9 percent for wages over $200,000 (individual) or $250,000 (couple), whereas the Social Security payroll tax is 12.4 percent.[18] When combined with the federal income tax, eliminating the contribution and benefit base would increase the top marginal tax rate to 46 percent on wage earners and 52 percent on the self-employed.[19] Including state and local income taxes would increase these amounts as much as 13 percentage points (e.g., 59% and 65% in California).[20] Marginal tax rates at such levels would likely have adverse effects on the economy and generate less revenue than expected.

Removing the limit on wages subject to the Medicare payroll tax does not provide a rationale for removing the limit for Social Security because the programs are fundamentally different in terms of benefit structure and sources of funding.

Payroll Taxes vs Income Taxes

Eliminating the contribution and benefit base for Social Security would increase payroll taxes, although not as much as expected, and it would also decrease income taxes. Thus, the net effect on total revenue would be less favorable to the overall federal budget.

The Social Security payroll tax is divided equally between workers and their employers with each paying 6.2 percent, for a total of 12.4 percent. Although half the tax is ostensibly paid by the employer, most economists agree workers bear the entire burden in the form of lower wages.[21] Thus, eliminating the contribution and benefit base would reduce wages by an amount equal to the employer share of the payroll tax.

For example, total wages covered by Social Security in 2022 were $10.3 trillion, with $8.7 trillion of that amount below the taxable maximum. Removing the limit would increase payroll taxes by nearly $200 billion per year, assuming no offsetting effects.[22] However, assuming employers offset their share of the additional payroll taxes by reducing their workers’ wages, payroll taxes and income taxes would be reduced by $44 billion, resulting in a net revenue increase of $155 billion.[23]

In the case of self-employed workers, removing the limit would increase payroll taxes by nearly $40 billion, but reduce federal income taxes by $6 billion due to their ability to deduct the additional payroll taxes from their taxable income.[24]

These estimates assume removing the limit on taxable wages has no impact on the decision of workers to either earn or report taxable income. They are “static” rather than “dynamic” estimates. However, there are likely to be additional adverse effects on the economy that would further reduce the total amount of revenue collected, although there would still be a net increase.[25] A comprehensive dynamic analysis is beyond the scope of this issue brief.

Social Security vs Medicare

Social Security is an enormously important and popular program. But it’s not the only program facing a long-term financial shortfall. Removing the limit on taxable wages for Social Security would represent a major new financial commitment to the program, and yet it would still fall short of providing the resources needed to fully fund the program. Moreover, removing the limit for Social Security would preclude the government from using the additional revenue to address the much larger shortfall in Medicare.

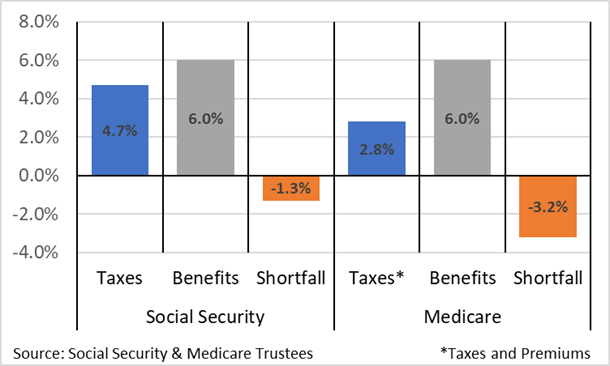

Under current law, the annual cost of both Social Security and Medicare is projected to be 6 percent of gross domestic product (GDP) by the year 2050. However, the amount of taxes and premiums dedicated to Medicare are significantly less than the amount of taxes dedicated to Social Security. As a result, the Medicare shortfall is nearly 2.5 times bigger than the Social Security shortfall, as shown in Figure 3.[26]

Figure 3: Social Security and Medicare as Percent of GDP in 2050

Removing the limit on taxable wages for Social Security would increase payroll taxes by nearly 1 percent of GDP, which would cover 70 percent of the Social Security shortfall in 2050, assuming no additional benefits are paid on wages above the limit.[27] Eliminating the shortfall in both programs would require not only removing the limit on taxable wages, but it would also require an increase in the combined Social Security and Medicare payroll tax rate from 15.3 percent to 20.6 percent.[28]

Congress is unlikely to address the entire Social Security and Medicare shortfall by only raising taxes. Nevertheless, these figures reveal that removing the limit on taxable wages for Social Security would be insufficient to eliminate the combined shortfall without also increasing the combined payroll tax rate by more than one-third.

Conclusion

Public opinion polls support the view that higher wage workers should pay more taxes to fund Social Security. However, this view overlooks the fact that the limit on taxes also serves as a limit on benefits. Without this limit, higher wage workers would pay unlimited taxes and receive unlimited benefits. The additional benefits would offset much of the additional taxes. To avoid this result, the limit on taxes could be eliminated while still maintaining the limit on benefits.

However, breaking the link between taxes and benefits would undermine the concept that Social Security is a universal program in which workers earn their benefits through a lifetime of contributions. Higher wage workers would receive no benefits for their additional contributions, while lower wage workers would receive benefits that would otherwise be unfunded for which they made no contributions.

Finally, removing the limit on Social Security payroll taxes would result in significantly higher marginal tax rates that could adversely affect the economy, reduce federal income tax receipts, and limit the funds available for Medicare. Policymakers should be aware of these unintended effects in their efforts to address the Social Security shortfall.

____________________________________________________________________________________________________

[1] Large Majorities of Republicans and Democrats Agree on Steps to Drastically Reduce Social Security Shortfall | Program for Public Consultation; Layout 1 (nasi.org); The Big Generation Gap at the Polls Is Echoed in Attitudes on Budget Tradeoffs | Pew Research Center; dfp_june22_ss_updated_tabs.pdf (filesforprogress.org)

[2] Contribution and Benefit Base | (ssa.gov)

[3] Social Security History | (ssa.gov) “We recommend that the contributory annuity system include, on a compulsory basis, all manual workers and nonmanual workers earning less than $250 per month, except those of governmental units and those covered by the United States Railroad Retirement Act.”

[4] Historical Statistics of the United States, Colonial Times to 1970 (census.gov) Series D 722-727

[5] Policymaking for Social Security | (brookings.edu) pp. 280-287

[6] IF11824 (congress.gov) Social Security currently covers about 94% of all workers.

[7] Cost-Of-Living Adjustments | (ssa.gov)

[8] Contribution and Benefit Base Determination | (ssa.gov)

[9] These figures represent the average indexed monthly earnings (AIME) and the primary insurance amount (PIA) for a worker earning the maximum taxable wage from age 22 (1983) until age 62 (2023). See Social Security Replacement Rates: “Nudging” in the Wrong Direction? – The Concord Coalition (Appendix).

[10] The Concord Coalition calculations based on data from the Social Security Administration, Long Range Solvency Provisions | (ssa.gov); and the Congressional Budget Office, Social Security Policy Options, 2015 | (cbo.gov)

[11] For a discussion of the implications of the buildup and depletion of the trust fund, see History and Future of the Social Security Trust Fund: Part III – The Concord Coalition

[12] History and Future of the Social Security Trust Fund, Part I – The Concord Coalition

[13] 2023 Medicare Trustees Report | (cms.gov) (Table III.B.2)

[14] Parts of Medicare | (ssa.gov)

[15] 2023 Medicare Trustees Report | (cms.gov) (Table IV.C.1); Your health plan options | Medicare

[16] Social Determinants of Health and Geographic Variation in Medicare per Beneficiary Spending | JAMA Network These figures use standardized (“price-adjusted”) payment rates to highlight differences in utilization, rather than differences in reimbursement, thereby understating the variation in spending between counties.

[17] Medical Expenditure Panel Survey (MEPS) Household Component (HC) | (ahrq.gov) See the “Use, Expenditures, Population” cross-sectional data for perceived health status and source of payment.

[18] Topic No. 560, Additional Medicare Tax | (irs.gov)

[19] [37% + 6.2% + 1.45% + 0.9%] on wages, or [37% + 15.3%*(1-7.65%) + 0.9%] on net earnings from self-employment. 2023 Schedule SE (Form 1040) | (irs.gov); 2023 Form 8959 | (irs.gov); IRS 2023 | (irs.gov)

[20] 2023 State Income Tax Rates and Brackets | Tax Foundation

[21] The Distribution of Household Income in 2020 | (cbo.gov), page 23

[22] Annual Statistical Supplement, 2023 – OASDI Covered Workers (4.B) | (ssa.gov) ($10,309 – $8,699) * 12.4% = $199.6 (in billions)

[23] ($10,309 – $8,699) * (1 – 6.2%) * 12.4% = $187.3 and ($199.6 – $187.3) / 12.4% * 32% = $32 billion, thus $199 – $187 – $32 = $44 (in billions), assuming a weighted average marginal tax rate of 32% on wages above the taxable maximum, see Wage Statistics for 2022 | (ssa.gov)

[24] Annual Statistical Supplement, 2023 – OASDI Covered Workers (4.B) | (ssa.gov) ($816 – $470) * (1-7.65%) * 12.4% = $39.6 / 2 * 30% = $5.9 (in billions), assuming a weighted average marginal tax rate of 30% on the deductible portion of the self-employment taxes above the taxable maximum, see SOI Tax Stats – Individual Statistical Tables by Size of Adjusted Gross Income | (irs.gov) (Table 1.4)

[25] How the Supply of Labor Responds to Changes in Fiscal Policy | (cbo.gov); Increase the Maximum Taxable Earnings That Are Subject to Social Security Payroll Taxes | (cbo.gov)

[26] 2023 OASDI Trustees Report – Table VI.G4.| (ssa.gov); Trustees Report & Trust Funds | CMS, Expanded and Supplementary Tables and Figures (ZIP)

[27] Ibid; Long Range Solvency Provisions | (ssa.gov)

[28] The Concord Coalition calculations based on SSA data assuming there would be a reduction in Social Security benefits proportional to the reduction in wages resulting from the increased employer share of the payroll tax. The calculation does not include the amount needed to offset the reduction in federal income taxes. Annual Statistical Supplement, 2023 – OASDI Covered Workers (4.B) | (ssa.gov)

Continue Reading